As the fourth quarter earnings season for ad software stocks wraps up, let’s take a look at the best and worst performers this quarter, including PubMatic ( NASDAQ:PUBM ) and its competitors.

The digital advertising market is large, growing and becoming increasingly diverse, both in terms of audience and media. As a result, there is a growing need for software that allows advertisers to use data to automate and optimize ad placement.

6 adware stocks we track reported good Q4; on average, revenue beat analyst consensus estimates by 3%, while revenue guidance for the next quarter was 1.4% above consensus. Stocks have faced challenges as investors prioritize short-term cash flow, but advertising software stocks have held up better than others, with share prices up an average of 13.5% from prior earnings results.

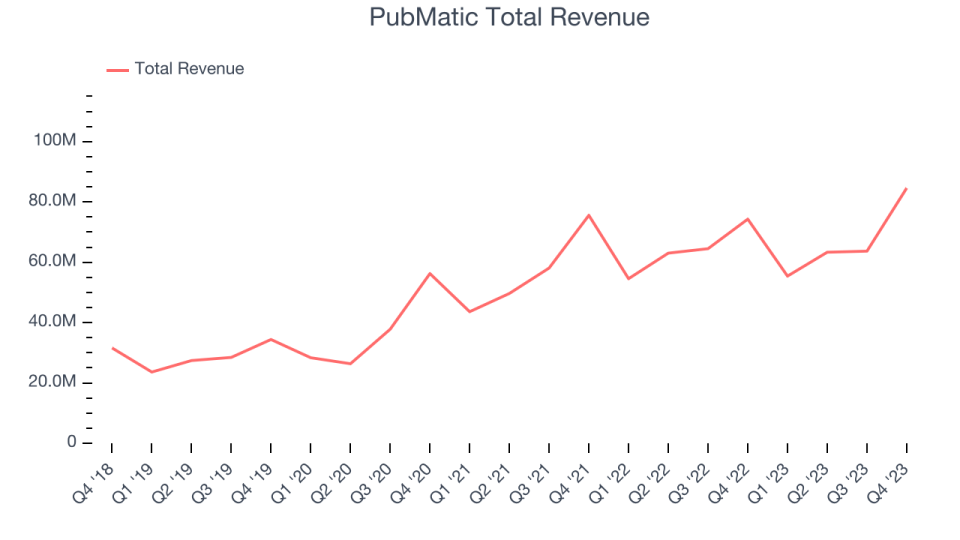

Top Q4: PubMatic (NASDAQ:PUBM)

Founded in 2006 as an online ad platform to help ad sellers, Pubmatic (NASDAQ: PUBM ) is a fully integrated, cloud-based programmatic advertising platform.

PubMatic reported revenue of $84.6 million, up 13.9% year-over-year, beating analysts’ expectations by 8.2%. It was a stunning quarter for the company, with significant gross margin improvement and upbeat revenue guidance for next quarter.

“We ended 2023 on an incredibly high note, marking an inflection point in revenue growth as we accelerated 14% year-over-year growth and strong profitability in the fourth quarter. These results highlight the strength of our platform, the value we deliver to publishers and customers, our focused investments in key areas of the business over the past 18 months, and the growing importance of sell-side technology across the ecosystem,” said Rajeev Goel. , co-founder and CEO of PubMatic.

According to analysts’ estimates, PubMatic achieved the highest result of the entire group. The stock is up 43.2% since the results and is currently trading at $23.72.

Is now the time to buy PubMatic? Access our full earnings performance analysis here, it’s free.

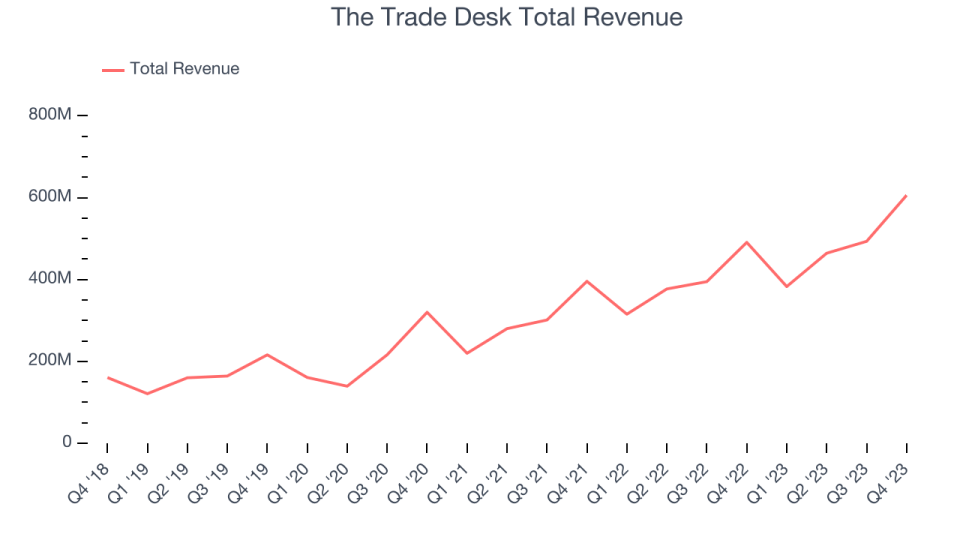

The Trade Desk (NASDAQ:TTD)

Founded by former Microsoft engineers Jeff Green and Dave Pickles, The Trade Desk (NASDAQ:TTD) offers cloud-based software that uses data to help advertisers better plan, place and target their online ads.

Trade Desk reported revenue of $605.8 million, up 23.4% year-over-year, beating analysts’ expectations by 4%. It was an impressive quarter for the company, with upbeat revenue guidance for next quarter and solidly better analysts’ billing estimates.

The stock is up 15.3% since the results and is currently trading at $87.3.

Is now the time to buy The Trade Desk? Access our full earnings performance analysis here, it’s free.

Weakest Q4: DoubleVerify (NYSE:DV)

When Oren Netzer saw a digital ad for US Target while sitting in his Tel Aviv apartment, he knew there was an unsolved problem, so he started DoubleVerify (NYSE:DV), a provider of advertising solutions to businesses that helps verify ads, prevent fraud and brand safety.

DoubleVerify reported revenue of $172.2 million, up 28.9% year-over-year, in line with analyst expectations. It was a weak quarter for the company, and full-year revenue guidance fell short of analysts’ expectations. On the other hand, revenues in the quarter rose slightly and gross margin improved.

DoubleVerify had the weakest performance relative to analyst estimates and the weakest updated full-year guidance in the group. The stock is down 9.2% since the results and is currently trading at $35.64.

Read our full analysis of DoubleVerify’s results here.

Zeta (NYSE:ZETA)

Co-founded by former Apple CEO John Scully, Zeta Global (NYSE:ZETA) provides software and data analytics tools that help companies sell their products to billions of customers.

Zeta reported revenue of $210.3 million, up 20.1% year over year, beating analysts’ expectations by 1.3%. It was a mixed quarter for the company, with full-year revenue forecasts beating analysts’ expectations but a decline in its gross margin.

Zeta achieved the highest annual guidance increase among its peers. The company added 12 business clients paying more than $100,000 a year to bring the total to 452. The stock is up 1.6% on the results and is currently trading at $10.93.

Read our full, actionable report on Zeta here, it’s free.

LiveRamp (NYSE:RAMP)

Launched in 2011 as a spin-out of RapLeaf, LiveRamp (NYSE:RAMP) is a software-as-a-service provider that helps businesses better target their marketing by merging offline and online data about their customers.

LiveRamp reported revenue of $173.9 million, up 9.6% year-over-year, beating analysts’ expectations by 1.2%. It was a solid quarter for the company, with accelerated customer growth and full-year revenue guidance that beat analysts’ expectations.

LiveRamp had the slowest revenue growth among its peers. The company added 6 enterprise clients paying more than $1 million annually to bring the total to 105. The stock is down 17.8% since the results and is currently trading at $34.5.

Read our full report on LiveRamp here, which is helpful and free.

Join paid stock investor research

Help us make StockStory more useful to investors like you. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Apply here.